The home ownership rate dipped to 65.1 percent in the second quarter, falling to the lowest level since the fourth quarter of 1995, the Census Bureau reported Tuesday. The drop coincides with efforts by consumer groups and lawmakers to try to make home ownership more inclusive, particularly at a time when affordability is still high.

In 2004, the U.S. home ownership rate soared to a record 69.2 percent. But the home ownership rate will likely reach bottom at about 64 percent in the next year due to the high number of foreclosures in the pipeline and rise in rental homes, Capital Economics Inc. analysts predict.

Meanwhile, lawmakers and consumer groups are trying to make home ownership more within reach to more families.

For example, “regulators are close to proposing a softened version of a rule requiring banks to keep a stake in risky mortgages they securitize,” Bloomberg reports. “Lawmakers currently shaping housing finance are seeking to reduce the government's role in keeping rates affordable for riskier borrowers while ensuring home ownership is within reach of minorities and first-time buyers who could be needed to sustain the housing recovery as borrowing costs rise from record lows.”

First-time buyers and minorities have seen some of the largest declines in home ownership rates. For example, the home ownership rate for blacks dropped to 42.9 percent in the second quarter of this year, compared with nearly 50 percent in the second quarter of 2004. Meanwhile, first-time buyers -- who are often in their 20s or early 30s -- have been at a disadvantage because of limited assets to come up with down payments and trying to meet tighter underwriting standards.

While the industry wants to encourage home ownership, it is moving cautiously to avoid repeating past mistakes, in which exotic adjustable rate mortgages and low down payments fueled a large housing bubble that eventually caused about 7 million people to lose their homes to foreclosure.

Source: “Homeownership Rate at Its Lowest Since 1995,” Reuters (July 30, 2013) and “Efforts under way to boost low home ownership rate,” Bloomberg News (July 30, 2013)

Wednesday, July 31, 2013

Monday, July 29, 2013

Report: 26% of HAMP Borrowers Redefaulted, Rate Continues to Worsen

Upon closer

examination, the Home Affordable Modification Program (HAMP) has not helped as

many borrowers as it may seem, according to a report from Special Inspector General for the Troubled Asset Relief Program (SIGTARP).

HAMP, a government loan modification program created to prevent foreclosures, has provided about 1.2 million modifications to distressed borrowers since its inception in 2009.

Of those borrowers, 306,538 redefaulted after falling behind on their payments by three months, which means in actuality, 865,100 are still actively in the program, the taxpayer watchdog agency revealed.

Of the redefaulters, 22 percent have entered into the foreclosure process.

Source: DSNews 07/24/2013

HAMP, a government loan modification program created to prevent foreclosures, has provided about 1.2 million modifications to distressed borrowers since its inception in 2009.

Of those borrowers, 306,538 redefaulted after falling behind on their payments by three months, which means in actuality, 865,100 are still actively in the program, the taxpayer watchdog agency revealed.

Of the redefaulters, 22 percent have entered into the foreclosure process.

On the other hand, homeowners who received modifications in early 2013 have a redefault rate of less than 1 percent.

The report also found states with a smaller numbers of HAMP borrowers tended to have higher redefault rates. Mississippi, which has provided just over 4,500 HAMP modifications, has a redefault rate of 35 percent, the highest out of any other state.

Based on region, Western states averaged the lowest default rate of 21 percent and had the highest number of permanent modifications as group.

The report also found states with a smaller numbers of HAMP borrowers tended to have higher redefault rates. Mississippi, which has provided just over 4,500 HAMP modifications, has a redefault rate of 35 percent, the highest out of any other state.

Based on region, Western states averaged the lowest default rate of 21 percent and had the highest number of permanent modifications as group.

Source: DSNews 07/24/2013

Sunday, July 28, 2013

Margin Loans Help Buyers Close Deals

Margin loans for short-term financing can help potential home buyers get cash fast to close a deal or win a bidding war — and an increasing number of people are turning to them for a quick fix.

"A person with easy access to cash may have a leg up over someone who has to have long-term financing," explains Tucker Watkins, a private wealth adviser with wealth-management company Ameriprise Financial Inc.

The product offers some pricing benefits, as there are no closing costs, no property appraisal is required, there are no prepayment penalties, and borrowers do not have to make monthly interest payments. There also are tax benefits to consider, given that interest on a margin loan generally is tax-deductible. On the other hand, a buyer who cashes out stocks to make a down payment may have to pay capital-gains taxes.

"Avoiding capital gains is often a reason why someone may use a margin loan instead of selling a security," says Watkins.

Source: RealtorMag // "For Faster Cash, Buyers Live on the Margin," The Wall Street Journal (July 19, 2013)

"A person with easy access to cash may have a leg up over someone who has to have long-term financing," explains Tucker Watkins, a private wealth adviser with wealth-management company Ameriprise Financial Inc.

The product offers some pricing benefits, as there are no closing costs, no property appraisal is required, there are no prepayment penalties, and borrowers do not have to make monthly interest payments. There also are tax benefits to consider, given that interest on a margin loan generally is tax-deductible. On the other hand, a buyer who cashes out stocks to make a down payment may have to pay capital-gains taxes.

"Avoiding capital gains is often a reason why someone may use a margin loan instead of selling a security," says Watkins.

Source: RealtorMag // "For Faster Cash, Buyers Live on the Margin," The Wall Street Journal (July 19, 2013)

Saturday, July 27, 2013

Fannie: Fast Rise in Mortgage Rates Could Hurt

The rise in mortgage rates over the last couple of months has been “significant” and could hamper the housing recovery, economists note in Fannie Mae’s Economic Strategic Report for July. However, home sales so far have been little affected by the spikes, they say.

The 30-year fixed-rate mortgage has risen more than 110 basis points from the first week of May to the end of June. In early July, it started to ease somewhat. Still, the report says that despite the increases, rates are still near historical lows. It’s the sudden rise in such a short time that has been alarming, the economists note.

Mortgage applications for home purchases have fallen about 9 percent since early May, when the rise in rates began. However, pending home sales during that same period rose to the highest level in more than six years. Many of those sales, though, are in cash, which means they may be less tied to the rise in mortgage rates.

Fannie Mae economists predict that mortgage rates will continue a gradual rise and average 4.7 percent in the fourth quarter. That is about 40 basis points higher than economists had predicted a month ago.

Economists predict home sales will rise about 8 percent in 2013, and the median home price will be $189,000 for existing homes and $276,000 for new homes in the fourth quarter.

Source: RealtorMag // “Fannie Mae Expects Rates to Continue Higher,” Mortgage News Daily (July 22, 2013)

The 30-year fixed-rate mortgage has risen more than 110 basis points from the first week of May to the end of June. In early July, it started to ease somewhat. Still, the report says that despite the increases, rates are still near historical lows. It’s the sudden rise in such a short time that has been alarming, the economists note.

Mortgage applications for home purchases have fallen about 9 percent since early May, when the rise in rates began. However, pending home sales during that same period rose to the highest level in more than six years. Many of those sales, though, are in cash, which means they may be less tied to the rise in mortgage rates.

Fannie Mae economists predict that mortgage rates will continue a gradual rise and average 4.7 percent in the fourth quarter. That is about 40 basis points higher than economists had predicted a month ago.

Economists predict home sales will rise about 8 percent in 2013, and the median home price will be $189,000 for existing homes and $276,000 for new homes in the fourth quarter.

Source: RealtorMag // “Fannie Mae Expects Rates to Continue Higher,” Mortgage News Daily (July 22, 2013)

Friday, July 26, 2013

What To Expect From Housing In The Second Half Of 2013

The U.S. housing recovery continues to make gains.

New home sales have surged 38% since last year, hitting a five-year high in June, according to the newest figures from the Commerce Department. And despite a monthly drop in activity, sales of previously owned homes remain 15% higher than last year as well, according to the National Association of Realtors.

Source: Forbes 7.26.2013

New home sales have surged 38% since last year, hitting a five-year high in June, according to the newest figures from the Commerce Department. And despite a monthly drop in activity, sales of previously owned homes remain 15% higher than last year as well, according to the National Association of Realtors.

If housing in the first six months of 2013 could be summed up in one sentence, it would go something like this: Inventory is painfully tight, sales activity is surging and home prices have jumping.

Now real estate experts are sounding off on the trends that will help shape the sector in the second half of 2013. Here’s what you need to know.

We Are Not Re-inflating A Bubble

Home prices have clocked double-digit price appreciation this year. Prices across the 20 major U.S. metro markets were 12% higher in April than they were a year before, according to the S&P/Case-Shiller Home Price Index. Other indexes have registered similarly dramatic gains. The last time prices appreciated by double digits were during the last housing bubble, motivating to question whether a new bubble is beginning to inflate.

It isn’t. The current pace of growth, while certainly unsustainable for long term market health, is nothing to worry about just yet. “Prices are now rising as fast as they were during the bubble years, but they are still low relative to the levels where they were back then,” explains Jed Kolko, chief economist of Trulia , a San Francisco, Calif.-based real estate site.

He says prices are actually undervalued across most of the country, lower not just than their bubble-era peaks but also lower than their historical norms when adjusted for inflation.

“You can sort of think of it as we overshot on the way down and this is sort of a correction back to something more normal,” adds Mark Fleming, chief economist of CoreLogic, an Irvine, Calif.-based real estate data firm.

Economists do believe home prices will continue to climb throughout the rest of this year. CoreLogic projects 2013 will end with a 6% increase over 2012. And Altos Research, a Mountain View, Calif.-based firm that tracks real estate data in real time, believes 2013’s final tally will be even higher. “Based on the actual supply and demand data, we are looking at 12% year-over-year,” says Michael Simonsen, chief executive of Altos Research.

Still, it won’t last. They say several variables, including increased inventory and higher mortgage rates, will slow the pace growth, which to be clear, is expected to stay positive over the next several years.

More Homes Coming To Market

I’ve said it before. The abnormally tight inventory levels fueling the return of such frothy buyer practices as bidding wars and contingency-free offers will slowly begin to ease. Inventory – which hit a 12-year low earlier this year — is already starting to increase and economists believe that trend will continue despite the season.

In June, there were 7% less home for sale than a year earlier, according to Realtor.com, but the monthly numbers offer the forward-looking story. From May to June, inventory grew by 4%; last year that monthly increase was only 1%.

“We think inventory levels on a year-over-year basis will probably flatten out by the end of this year. That will be the first time since 2007,” says Errol Samuelson, president of Realtor.com. “I think you are actually going to see inventory growth on a year-on-year basis starting in the fall, but prices nonetheless will continue to appreciate.”

“Inventory started to expand very slowly maybe about four months ago,” echoes Kolko. “We will see that continue as rising prices help owners get back above water and help other sellers decide to take advantage of price appreciation.”

Still, some experts, like Simonsen, believe we could see housing shortages in the most sought after locales as far out as the next three years.

It will come down to new construction as more homebuilders continue to gain confidence and roll new developments. Kolko expects to see more construction commence in places like Texas, the Carolinas, Northern California and other parts of country where there’s strong housing demand, spurring job growth in both construction and housing-related industries.

Since an unusually large portion of new construction is multifamily, increased inventory won’t just help slow the rapid rate of home price growth but also quell rent prices. As many as six million more households will join the rental market ranks over the next decade, according to the National Association of Realtors; more building in major cities will help keep rents from rising too much in response.

Mortgage Rates Will Keep Climbing

Mortgage rates have risen over the past two months. A recent Trulia survey found rising rates was the number one worry among prospective buyers right now.

Economists believe rates will continue to climb, though at a much less feverish pace than recently witnessed. But while the higher rates – the 30-year fixed loan is about a point higher than it was in early May – mean borrowing is getting more expensive, housing won’t become unaffordable anytime soon.

“Prices are still low relative to rents, so at 4.5%, it’s still more than a third cheaper to buy than to rent on average across the U.S.,” notes Kolko. “Not every market will remain cheaper to buy but on average… buying will stay cheaper than renting until rates reach 10.5% — a level we haven’t seen since 1990.”

Still, in metro areas like San Francisco, San Jose, New York and Honolulu, markets that were always historically cheaper to rent than buy before the downturn, rates will begin to tip the scale back toward renting once they rise above 5%.

“Our estimation is it would take a 6.5% interest rate to bring affordability just back up to the level of early 2000s, [meaning] neither too affordable nor unaffordable,” adds CoreLogic’s Fleming. “There’s plenty of room for appreciation and rate increases before that and we will probably get a little of both.”

Rising rates may help fuel another trend in the coming months: an easing of tight mortgage credit that has hampered the purchases of even qualified homebuyers. As rates rise, refinancing business dries up, pushing lenders to begin ramping up the mortgages they underwrite for prospective buyers.

Distressed Decline

Foreclosure activity is on the decline. RealtyTrac, an Irvine, Calif.-based foreclosure site, reports that 800,000 properties had foreclosure filings on them nationwide in the first half of 2013. That’s down 19% from the second half of 2012 and down 23% from the six months before that. In June there were 127,000 filings across the U.S. – the lowest number logged since December 2006.

“On a nationwide basis we will continue to see the numbers go down,” projects Daren Blomquist, vice president of RealtyTrac. “We will still have the flare-ups in state and local markets…but nothing that is going to overwhelm the momentum we have in the market right now.”

He says the exceptions to that downward trend will continue to be states where foreclosures undergo a judicial process. Florida, New York, New Jersey, Illinois, and Maryland has all seen increases in activity this year, in part because lenders are finally dealing with distressed inventory that had been delayed. Another market that may experience a “last gasp” of foreclosures is California, since the state’s Homeowner Bill of Rights has slowed down the foreclosure process.

Short sales continue to increase, with lenders arranging deals before they even process their first foreclosure filing on a delinquent homeowner’s property. In the first quarter of 2013 short sales increased 79% versus a year earlier, thanks in part to the fact that short sale guidelines were loosened by the government sponsored enterprises.

Another trend that will continue: investor activity, especially among institutions. Institutional investors funded by Wall Street capital have been buying up distressed single family homes and converting them into rentals. According to RealtyTrac’s data, which defines institutional investors as entities that have purchased 10 or more properties in the past year, purchases have continued to increase, with southeastern markets like Florida and Georgia logging 200%-plus yearly increases.

“The one big pool of risk is the underwater homeowners,” says Daren Blomquist, vice president of RealtyTrac, an Irvine, Calif.-based foreclosure site. He estimates that there are as many as 11.3 million borrowers holding mortgage notes worth more than their homes. “It’s going to take two or three years before they actually have equity in their homes. Until we have those people in a place where they can participate in the market, there will be a slight drag on the housing market.”

Source: Forbes 7.26.2013

10 Metros Where Rents Are Soaring

Investors eager to pick up rental properties should be eyeing several metros, particularly out West, where rental rates have skyrocketed over the past year.

The San Francisco Bay Area has seen some of the largest rent hikes — an increase of 7.8 percent in the second quarter of this year compared to the same time period a year ago, according to Texas-based market-research firm MPF Research.

Of the top 50 U.S. metros with the highest average rent growth, the following areas have seen the biggest spikes, MPF found:

The San Francisco Bay Area has seen some of the largest rent hikes — an increase of 7.8 percent in the second quarter of this year compared to the same time period a year ago, according to Texas-based market-research firm MPF Research.

Of the top 50 U.S. metros with the highest average rent growth, the following areas have seen the biggest spikes, MPF found:

- San Francisco: 7.8%

- Oakland, Calif.: 6.9%

- Denver: 6.1%

- Seattle: 6%

- San Jose, Calif.: 5%

- Portland, Ore.: 4.4%

- Houston: 4.3%

- Austin, Texas: 4.1%

- West Palm Beach, Fla.: 4%

- Fort Worth, Texas: 3.6%

Thursday, July 25, 2013

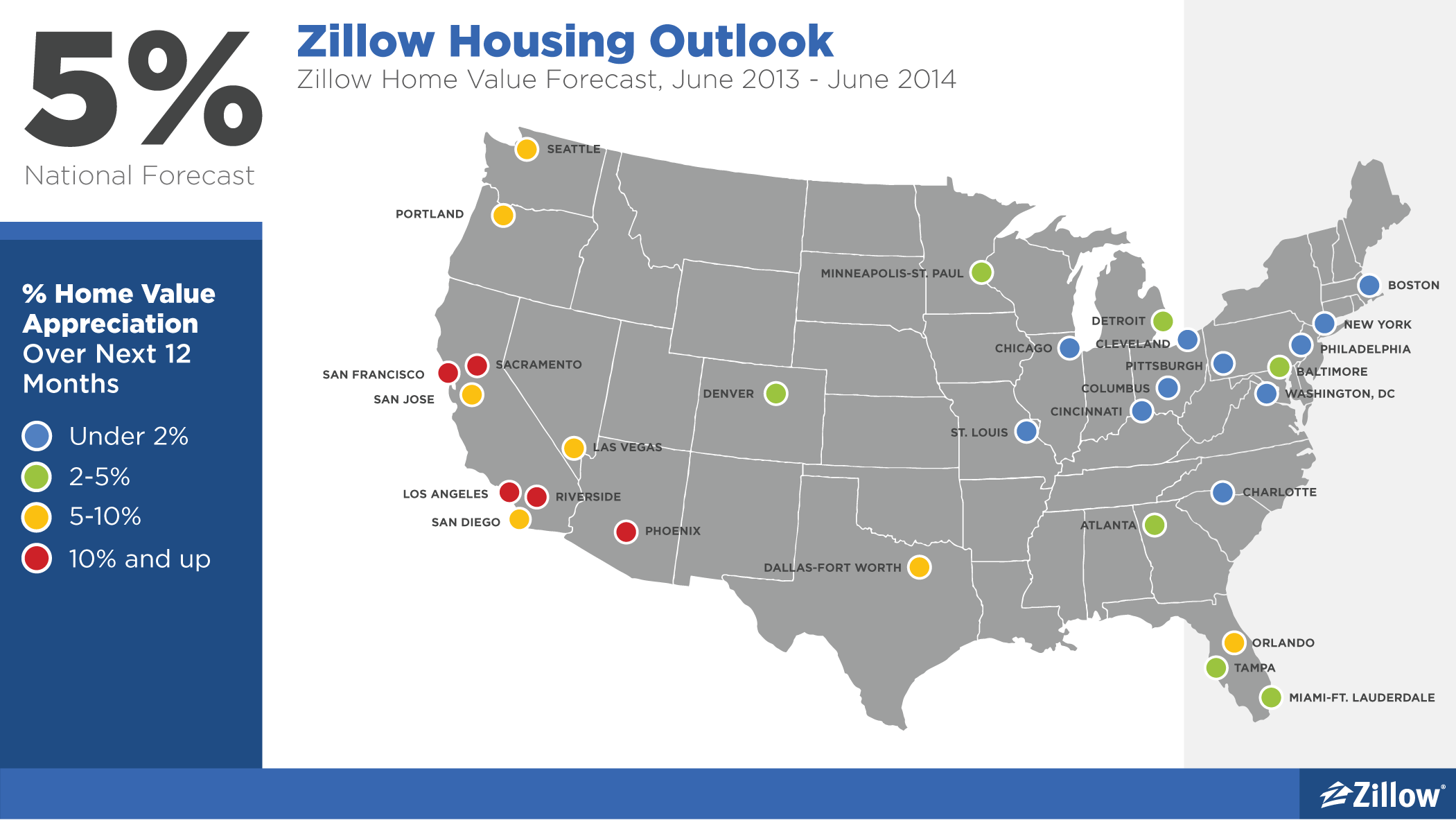

2013 Spring Selling Season - Hottest Since 2004, As Recovery Accelerates & Widens

Overview

Zillow’s second quarter Real Estate Market Reports , released today, show home values increased 2.4% from the first quarter of 2013 to the second quarter of 2013 to $161,100. This quarter marks the largest annual gain since August 2006 and largest quarterly gain since the fourth quarter of 2005. On an annual basis, the Zillow Home Value Index (ZHVI) rose 5.8% from June 2012 levels.Monthly appreciation remains strong with national home values growing by 0.9% from May. Not only did the pace of home value appreciation quicken in the second quarter, but the recovery also fully took hold nationwide. Markets in some areas of the Northeast, Midwest and Southeastern U.S., such as Atlanta, Chicago and St. Louis, that had previously been slow to turn the corner began to appreciate, which helped boost the overall national market.

All of the top 30 largest metro areas covered by Zillow experienced annual appreciation in home values as of the end of the second quarter, and all have hit their bottom.

{kind=link}

According to the Zillow Home Value Forecast, we expect national home values to increase 5% over the next year (June 2013 to June 2014). Of the 257 markets covered by the Zillow Home Value Forecast, 241 markets are expected to see increases in home values over the next year, with the largest increases expected in the Sacramento metro (18.9%) and the Riverside metro (16.6%).

Many California markets follow closely at the top of the list of markets expected to see the highest home value appreciation over the next year. According to the Zillow Home Value Forecast, 234 markets (91%) have already hit a bottom in home values, and another 13 are expected to hit a bottom by June 2014.

Home Values

The Zillow Real Estate Market Reports cover 389 metropolitan and micropolitan areas (metros) of which 259 showed quarterly home value appreciation. Three metros remained flat, while 127 metros show home values losses.Approximately 72% of the metros covered by the Real Estate Market Reports posted annual increases in home values – a sign of the national housing recovery continuing to take hold. Among the largest metros, Sacramento showed the largest annual increase with home values rising 29.5% from the second quarter of 2012 to the second quarter of 2013.

We do believe that appreciation rates will return to more sustainable levels over the next year or two. Overall, national home values are back to August 2004 levels, down 17.2% since their peak in May 2007. A table of the top 30 metros can be found at the end of this report.

Rents

The Zillow Rent Index (ZRI) covers 496 metro areas, and 57% of those metros reported annual increases in rents in June. As a point of comparison, nearly 72% of the metro areas covered by the ZHVI experienced annual home value increases. Nationally, rents increased 1.6% in June from year-ago levels, denoting a slowing. This is a significant annual decline in the rental appreciation rate from its peak appreciation of 6.2% nationally in September 2012. This development combined with rising home values is another contributor to investors exiting some markets as they had often bought for-sale inventory to convert them to for-rent properties. Markets that continue to see extremely strong year-over-year rent increases include Cincinnati (10.5%), Denver (5.5%) and Boston (4.3%).Foreclosures

The rate of homes foreclosed continued to decline in June with 4.96 out of every 10,000 homes in the country being liquidated through foreclosure. Nationally, foreclosure resales remain low, making up 9.53% of all sales in June, down 3.6 percentage points from the second quarter of 2012, underlining the limited inventory of foreclosure resales. For-sale inventory levels remain constrained, with manymetro areas across the country having fewer for-sale listings available in June compared with last year, although constraints are beginning to ease. The lack of foreclosure resales and normal for-sale inventory in many markets is contributing to home value appreciation. In the second half of the year we expect continued easing with investors starting to slowly exit markets as home values continue to climb.

Outlook

With the housing recovery in full force, many homeowners are feeling a sense of whiplash after years of depreciation, but this kind of market behavior won’t last. Investors are starting to pull out of some markets – as home values are climbing higher – and regular buyers are coming back, now that they can be competitive again. Although, some consumers are starting to feel the decrease in purchasing power due to higher mortgage rates.More for-sale inventory is slowly but surely coming on line, as homes are freed from negative equity and more homeowners are deciding to sell. Both of these developments will contribute to slowdowns in appreciation toward more sustainable rates.

In some overheated markets, rapid home value increases coupled with rising mortgage rates will lead to housing prices and financing costs outpacing local income growth, which will also contribute to a moderation of the market.

The U.S. housing market as a whole is currently not experiencing a bubble, but in many places it may feel like one, with some markets (Sacramento, Las Vegas, San Francisco) experiencing annual home value appreciation approaching 30 percent.

Source: Zillow Real Estate Research

Wednesday, July 24, 2013

U.S. House Prices Climbed 7.3% in Year Through May

U.S. house prices rose 7.3 percent in the year through May as buyers competed for a small supply of listings, according to the Federal Housing Finance Agency.

Prices increased 0.7

percent on a seasonally adjusted basis from April, the FHFA said in a report

today from Washington. The average economist estimate was for a 0.8

percent gain, according to data compiled by Bloomberg.

Real estate values are climbing as improving employment helps

draw buyers into the market for a tight inventory of homes. A separate report

today from Zillow Inc. (Z) showed

U.S. home values rose 2.4 percent in the second quarter from the previous three

months. It was the biggest gain for a second quarter since 2004.

“The U.S. housing market as a whole is currently not experiencing a bubble, but

in many places it sure must feel like one,” Zillow Senior Economist Svenja

Gudell said in a statement. “Homeowners are feeling a sense of whiplash after

years of depreciation.”

The limited supply and

higher mortgage rates may be restraining purchases. Sales of previously owned homes unexpectedly slipped 1.2 percent in

June to 5.08 million annualized rate, the National Association of Realtors

reported yesterday. The number of properties on the market last was month was

the fewest for any June since 2001.

Market ‘Excitement’

The average rate for a 30-year fixed loan was 4.37 percent last week, up from a near-record low of 3.35 percent in May, according to Freddie Mac.“Our inventory is incredibly low right now,” Margaret Kelly, chief executive officer of Re/Max LLC, a Denver-based network of real estate agencies, said on Bloomberg Television’s “Market Makers” with Sara Eisen and Deirdre Bolton. “When you have low inventory, high demand, prices rise, you’ve got a lot of excitement in the market. I think once we see inventory rise a bit, you’re going to see some of those things calm down. It’ll be more of a normal market.”

The FHFA’s report showed prices

increased 15.8 percent from a year earlier in the Pacific area, which includes

California and Oregon. In the Mountain region, including Nevada and Arizona, the gain

was 12.7 percent. The East South Central area -- including Kentucky and Alabama -- had

the smallest increase, at 2.7 percent.

The FHFA index measures

transactions for single-family properties financed with mortgages owned or

securitized by Fannie Mae and Freddie

Mac. The gauge is 11.2 percent below its April 2007 peak.

Source: Bloomberg

Source: Bloomberg

Thursday, July 18, 2013

Forecast Points to Steady Price Growth Led by California

When it comes to price appreciation, California markets are expected to continue leading growth over the next year, while certain areas concentrated in the Northeast should see a decline in home values, according to Veros Real Estate Solutions’ most recent forecast ending June 1, 2014.

The company’s forecast covers 969 counties, 324 metro areas, and 13,502 zip codes.

In the next 12 months, Veros projects San Francisco will come out ahead with a 12.7 percent increase.

The predictive technology software company described San Francisco as having a “serious housing shortage,” combined with “historically good affordability” and a lower unemployment rate of 6.7 percent compared to the national average of 7.6 percent as of May.

Other metros in the top five for price appreciation are Los Angeles (+11.6 percent), San Jose (+11.1 percent), Midland, Texas (+11.1 percent), and Phoenix (+10.9 percent).

Among the top 100 markets, Veros’ home price index (HPI) projects a 3.1 percent increase, marking the fourth straight quarterly gain.

The company’s forecast covers 969 counties, 324 metro areas, and 13,502 zip codes.

In the next 12 months, Veros projects San Francisco will come out ahead with a 12.7 percent increase.

The predictive technology software company described San Francisco as having a “serious housing shortage,” combined with “historically good affordability” and a lower unemployment rate of 6.7 percent compared to the national average of 7.6 percent as of May.

Other metros in the top five for price appreciation are Los Angeles (+11.6 percent), San Jose (+11.1 percent), Midland, Texas (+11.1 percent), and Phoenix (+10.9 percent).

Among the top 100 markets, Veros’ home price index (HPI) projects a 3.1 percent increase, marking the fourth straight quarterly gain.

Wednesday, July 17, 2013

Report: Traditional Buyers Need to Fill the Widening Cash Buyer Void

If it wasn't for cash

sales during the housing downturn, sales today would look much weaker, and the

dramatic price declines over the past few years would have been even steeper,

CoreLogic reported Tuesday.

From 2000 to 2005, cash sales remained steady, representing around 25 percent of all sales. When the real estate market crashed in 2007 and 2008, the share of cash sales, driven by the rise in REO sales, jumped and eventually peaked above 40 percent two years ago.

While cash sales still remain elevated, they are past their prime point and are slowly fading. For 19 straight months now, cash sales have been declining.

CoreLogic also examined cash sale trends among the 10 largest markets.

According to the report, the idea that hardest hit markets have the largest share or increase in cash sales is a “myth.” For example, New York actually had the highest cash sales share at 53 percent, though hard-hit markets such as Riverside, California, and Phoenix also held high shares that exceeded 40 percent.

Interestingly, in some markets, investor activity has shifted from REO and short sales to non-distressed sales, leading an a surge in prices for non-distressed cash resales, CoreLogic explained.

The markets where prices for non-distressed cash sales increased the most year-over-year in April this year were Atlanta (+46 percent), Phoenix (+34 percent), and Riverside (+28 percent).

As cash sales wane with investor activity, the data provider pointed to the need for traditional and first-time buyers to play a bigger role in housing to help the recovery move forward.

However, CoreLogic concluded “rising rates and home prices will not dissuade the more traditional buyer from entering the market and financing a home purchase” since home affordability remains high and supply is increasing.

From 2000 to 2005, cash sales remained steady, representing around 25 percent of all sales. When the real estate market crashed in 2007 and 2008, the share of cash sales, driven by the rise in REO sales, jumped and eventually peaked above 40 percent two years ago.

While cash sales still remain elevated, they are past their prime point and are slowly fading. For 19 straight months now, cash sales have been declining.

CoreLogic also examined cash sale trends among the 10 largest markets.

According to the report, the idea that hardest hit markets have the largest share or increase in cash sales is a “myth.” For example, New York actually had the highest cash sales share at 53 percent, though hard-hit markets such as Riverside, California, and Phoenix also held high shares that exceeded 40 percent.

Interestingly, in some markets, investor activity has shifted from REO and short sales to non-distressed sales, leading an a surge in prices for non-distressed cash resales, CoreLogic explained.

The markets where prices for non-distressed cash sales increased the most year-over-year in April this year were Atlanta (+46 percent), Phoenix (+34 percent), and Riverside (+28 percent).

As cash sales wane with investor activity, the data provider pointed to the need for traditional and first-time buyers to play a bigger role in housing to help the recovery move forward.

However, CoreLogic concluded “rising rates and home prices will not dissuade the more traditional buyer from entering the market and financing a home purchase” since home affordability remains high and supply is increasing.

Monday, July 15, 2013

Underwater Home Owners Not Being Held Back, Study Says

Underwater home owners are willing to move, despite losing money on their homes, new research shows.

In fact, home owners who owe more on their mortgage than their home is currently worth are more willing to move away if a job opportunity arises than even home owners with equity, according to researchers with the Federal Reserve Bank of Cleveland. The research, based on data from credit bureaus, aims to debunk a popular theory that underwater home owners have been held back by their lack of equity status. Dubbed the “lock-in effect,” the theory suggests that those with negative equity have avoided moving for a job due to being underwater.

The latest research shows that home owners with homes worth less than 80 percent of their mortgage debt were one percent more likely to move for a new job in a given year compared to those who held 20 percent of equity in their homes.

"If a hypothetical unemployed, underwater home owner gets a job offer, he is going to take it," says reearcher Yuliya Demyanyk.

"An implication for national policymakers is that job creation efforts need not focus on the regions hit hardest by the housing bust. Consider that at the end of 2009, the underwater problem was concentrated in four sand states — Arizona, Florida, California, and Nevada — and in Michigan, all with negative equity rates topping 35 percent of total mortgages," Demyanyk writes in the research paper. "If national policymakers thought only about creating jobs in those states out of fear that negative-equity borrowers wouldn’t move to other states for employment, they might be missing an opportunity to lift employment more broadly."

In fact, home owners who owe more on their mortgage than their home is currently worth are more willing to move away if a job opportunity arises than even home owners with equity, according to researchers with the Federal Reserve Bank of Cleveland. The research, based on data from credit bureaus, aims to debunk a popular theory that underwater home owners have been held back by their lack of equity status. Dubbed the “lock-in effect,” the theory suggests that those with negative equity have avoided moving for a job due to being underwater.

The latest research shows that home owners with homes worth less than 80 percent of their mortgage debt were one percent more likely to move for a new job in a given year compared to those who held 20 percent of equity in their homes.

"If a hypothetical unemployed, underwater home owner gets a job offer, he is going to take it," says reearcher Yuliya Demyanyk.

"An implication for national policymakers is that job creation efforts need not focus on the regions hit hardest by the housing bust. Consider that at the end of 2009, the underwater problem was concentrated in four sand states — Arizona, Florida, California, and Nevada — and in Michigan, all with negative equity rates topping 35 percent of total mortgages," Demyanyk writes in the research paper. "If national policymakers thought only about creating jobs in those states out of fear that negative-equity borrowers wouldn’t move to other states for employment, they might be missing an opportunity to lift employment more broadly."

Source: Realtor Mag // “Fed researcher: Underwater homes are not holding jobseekers back,” HousingWire (July 11, 2013)

ASKING PRICES UP YEAR-OVER-YEAR NATIONWIDE

Nationally, asking prices on for-sale homes rose 10.7 percent

year-over-year in June, according to the Trulia Price Monitor. Even

excluding foreclosures, prices jumped 11.4 percent year-over-year, signaling

that the current rise in prices is not primarily driven by the shift away from

foreclosure to non-distressed homes for sale. However, asking prices will

eventually slow down as mortgage rates rise, inventory expands, and investor

demand falls.

Nationally, asking home prices bottomed in February 2012 – but the turnaround has been uneven. Prices first rebounded two years ago in San Jose, Phoenix, Denver, Miami, and a few other housing markets where job growth or bargain buying started boosting prices earlier. Meanwhile, prices continued to fall in several East Coast and Midwest markets until three to six months ago. Now with the housing recovery in full swing, asking prices rose in 99 of the 100 largest metros. Among these recently bottoming markets, prices rose more than 7 percent in Edison-New Brunswick, NJ, Chicago, Lake County-Kenosha County, IL-WI, and Baltimore.

Source: Trulia

Nationally, asking home prices bottomed in February 2012 – but the turnaround has been uneven. Prices first rebounded two years ago in San Jose, Phoenix, Denver, Miami, and a few other housing markets where job growth or bargain buying started boosting prices earlier. Meanwhile, prices continued to fall in several East Coast and Midwest markets until three to six months ago. Now with the housing recovery in full swing, asking prices rose in 99 of the 100 largest metros. Among these recently bottoming markets, prices rose more than 7 percent in Edison-New Brunswick, NJ, Chicago, Lake County-Kenosha County, IL-WI, and Baltimore.

Source: Trulia

Sunday, July 14, 2013

Nation's Largest Investor Says They're Not Done Buying Yet

Blackstone Real Estate, the nation’s largest owner of single-family homes, says they’re not done buying homes yet. Jonathan Gray, Blackstone’s global head of real estate, says that prices are still low in many areas and it’s still an opportunistic time for real estate investors.

"In places like California it has gotten more difficult, but as you move East ... Atlanta, Chicago, Northern Florida—we still see good value," Gray told CNBC.

Prices are still very much below 2006 levels in many areas, Gray notes. “We think they still represent good value, and the supply-demand picture there looks pretty good,” Gray says. “We’ve only been building at about half the rate of obsolescence and population growth in terms of new starts, and that is supporting the value.”

Gray says he expects the single-family housing market to remain bullish for two to four more years.

Blackstone Real Estate’s portfolio is made up of 31,000 homes in 13 housing markets across the country. The company renovates the properties and leases them. The company has about a 94 percent occupancy rate on the homes it owns.

"In places like California it has gotten more difficult, but as you move East ... Atlanta, Chicago, Northern Florida—we still see good value," Gray told CNBC.

Prices are still very much below 2006 levels in many areas, Gray notes. “We think they still represent good value, and the supply-demand picture there looks pretty good,” Gray says. “We’ve only been building at about half the rate of obsolescence and population growth in terms of new starts, and that is supporting the value.”

Gray says he expects the single-family housing market to remain bullish for two to four more years.

Blackstone Real Estate’s portfolio is made up of 31,000 homes in 13 housing markets across the country. The company renovates the properties and leases them. The company has about a 94 percent occupancy rate on the homes it owns.

Source: Realtor Mag

Saturday, July 13, 2013

Report: Shadow Inventory Falls 34% from 2010 Peak

Fewer than 2 million homes remain in shadow inventory as of April, CoreLogic reported Tuesday.

This puts shadow inventory at a supply of 5.3 months and represents an 18 percent year-over-year decrease. The data provider also reported shadow inventory is 34 percent lower than the 2010 peak of 3 million. For its estimate, CoreLogic counts unlisted properties that are seriously delinquent, in foreclosure, or held as REOs as shadow inventory.

Currently, serious delinquencies make up the bulk of shadow inventory. Out of the total for shadow inventory, about 890,000 homes are seriously delinquent, while 761,000 are in some stage of foreclosure, and another 336,000 are REOs.

However, serious delinquencies, or mortgages past due by 90 days or more, are trending downward, falling to under 2.3 million in May, which represents 5.6 percent of mortgages.

Currently, serious delinquencies make up the bulk of shadow inventory. Out of the total for shadow inventory, about 890,000 homes are seriously delinquent, while 761,000 are in some stage of foreclosure, and another 336,000 are REOs.

However, serious delinquencies, or mortgages past due by 90 days or more, are trending downward, falling to under 2.3 million in May, which represents 5.6 percent of mortgages.

“The stock of seriously delinquent homes, which is the main driver of shadow inventory, is at the lowest level since December 2008,” said Dr. Mark Fleming, chief economist for CoreLogic. “Over the last year it has decreased in 42 states by double-digit figures, resulting in rapid declines in shadow inventory for the first quarter of 2013.”

The number of homes in foreclosure inventory, or in some stage of foreclosure, totaled 1 million in May, down 29 percent from a year ago and down 3.3 percent over the last month. As a percentage, foreclosure inventory represents 2.6 percent of mortgages, down from 3.5 percent in May 2012.

Completed foreclosures also experienced a steep annual decrease, falling to 52,000 in May, down 27 percent from a year ago when completed foreclosures totaled 71,000. From April to May, however, completed foreclosures increased, rising 3.5 percent from 50,000 in April.

The state that accumulated the most completed foreclosures over the last year was Florida, where 103,000 homes have been lost to foreclosure.

California came in at second, with 76,000 completed foreclosures, followed by Michigan (64,000), Texas (51,000), and Georgia (47,000).The five states alone account nearly half of all completed foreclosures, CoreLogic stated.

Florida was also in the lead for foreclosure inventory, with 8.8 percent of mortgages in foreclosure.

Also in the top five were New Jersey (6.0 percent), New York (4.8 percent), Maine (4.1 percent), and Connecticut (4.1 percent).

Source: DS News

The number of homes in foreclosure inventory, or in some stage of foreclosure, totaled 1 million in May, down 29 percent from a year ago and down 3.3 percent over the last month. As a percentage, foreclosure inventory represents 2.6 percent of mortgages, down from 3.5 percent in May 2012.

Completed foreclosures also experienced a steep annual decrease, falling to 52,000 in May, down 27 percent from a year ago when completed foreclosures totaled 71,000. From April to May, however, completed foreclosures increased, rising 3.5 percent from 50,000 in April.

The state that accumulated the most completed foreclosures over the last year was Florida, where 103,000 homes have been lost to foreclosure.

California came in at second, with 76,000 completed foreclosures, followed by Michigan (64,000), Texas (51,000), and Georgia (47,000).The five states alone account nearly half of all completed foreclosures, CoreLogic stated.

Florida was also in the lead for foreclosure inventory, with 8.8 percent of mortgages in foreclosure.

Also in the top five were New Jersey (6.0 percent), New York (4.8 percent), Maine (4.1 percent), and Connecticut (4.1 percent).

Source: DS News

Friday, July 12, 2013

Recovery Persists Despite Interest Rate Hikes

A recent survey conducted by Fannie Mae reveals that a clear majority of prospective homebuyers still believe it’s a good time to buy a home despite increasing interest rates on mortgages. A majority of people surveyed also believe home prices will continue to rise, which supports experts’ theories that most people are aware that the market is still good for buying when compared to previous years. Historical data reflect similar patterns regarding shifts in interest rates, which may also mean that interest rates don’t factor in as heavily as other indicators when people are considering a home purchase.

Buying a home has become more expensive because of rising home prices and interest rates, but it appears it would take more to shake the housing recovery.

In Fannie Mae's June National Housing Survey, 72% of the respondents said it was still a good time to buy a home, even though the share of respondents who expected mortgage rates to increase in the next 12 months rose by 11 percentage points to 57%, the highest level in the survey's three-year history.

The share of respondents who believe home prices will go up in the next year also hit a survey high of 57%, underlining consumers' confidence in the housing recovery.

"Consumers may recognize that today's still favorable mortgage rates and homeownership affordability levels will recede over time," said Fannie Mae economist Doug Duncan. "Given rising home and rental price expectations and improving personal financial attitudes, more prospective homebuyers may be deciding that now is the time to get off the fence."

Housing and mortgage analysts have also argued that the rise in interest rates, while denting affordability, is unlikely to deter the recovery. In fact, some have concluded that interest rates have only a limited impact on home prices.

In a report released Sunday, KBW analysts look at past behavior of home prices in the U.S. and in the state of California during periods of rising interest rates, starting from the 1980s.

Rising interest rates did not cause a drop in home prices as is commonly feared. In fact, the analysts found that historically rising home prices and rising interest rates went hand-in-hand.

This was because "early in a recovery period for home prices, positive economic growth and increasing demand for housing offset rising financing costs," they wrote.

Interest rates appeared to have a very small impact on home prices. For instance, between January 1993 and January 1995, interest rates moved from about 8% to a little over 9%. Home prices in the U.S. still rose, irrespective of the move in rates. In California, however, home prices declined, as the local economy was still climbing out of recession.

Between 2003 and 2007, similarly, home prices rose in both the U.S. and in California, while interest rates rose. Later, in 2007, prices plummeted during a time of declining interest rates.

"We are not attempting to draw a conclusion that higher mortgage rates support rising home values," the analysts emphasized in their report. "Rather we are suggesting that the direction of mortgage rates has little impact on the direction of home prices, as other factors, such as economic growth and home supply, are likely the key drivers of home price movements."

Indeed, while low interest rates have enabled many people to refinance or purchase homes, they are not the reason behind the rise in home prices. Rates were low for a long time after the bust, yet home prices went nowhere but down until March 2012.

Rather it was the decline in excess supply of homes that kickstarted the housing recovery.

For now, the supply of existing and new homes remains constrained, but it is expected to ease as more sellers list their homes and homebuilders ramp up construction.

This could moderate price gains, especially if mortgage credit standards remain tight, forcing more people to rent.

Source: NuWire Investor

Thursday, July 11, 2013

US Foreclosure Rates Falling

The newest report from CoreLogic shows that foreclosure activity dropped in May as the U.S. continues forward in its housing market recovery. The foreclosure inventory is also shrinking and seriously delinquent loans are at their lowest level since the end of 2008. Part of it is due to an improving economy and more positive activity in the housing sector, but it’s also because many banks have chosen to deal with delinquency by way of short sales and loan modifications rather than enter into costly foreclosures. Experts say the overall impact contributes to rising home prices and even more sales activity, further boosting the recovery.

Fewer homes were lost to foreclosure in May and the total number of homes in the foreclosure process continued to decline, according to the latest report from real estate analytics provider CoreLogic.

The number of completed foreclosures dropped 27% year-over-year in May to 52,000. Month-over-month, completed foreclosures rose 3.5%.

Completed foreclosures represent the number of homes actually lost to foreclosure. Since the crisis began in September 2008, there have been 4.4 million completed foreclosures. Prior to the crisis, completed foreclosures averaged 21,000 a month, less than half the current pace.

Still, the latest reports continue to support the view that the foreclosure crisis is slowly moving behind us.

The number of homes in some stage of foreclosure was about 1 million in May, down 29% year-over-year. Month-over-month, the foreclosure inventory was down 3.3%. About 2.6% of all homes with a mortgage were in some stage of foreclosure, compared to 3.5% a year earlier.

Seriously delinquent loans -- loans that 90 days or more past due -- are now at their lowest level since December 2008, at 2.3 million mortgages.

The decline in seriously delinquent loans is significant because a good proportion of these loans could ultimately end up in foreclosure if they are not resolved. And mounting foreclosures add to the supply of distressed homes in the market, dragging down home prices.

Homes that could potentially wind up in foreclosure represent "shadow inventory" or pending supply that could hit the market.

As of April, the shadow inventory was under 2 million, or 5.3 months' supply.

For a long time time shadow inventory was seen as a threat to the housing market. However, that view changed as banks began to opt for short sales and loan modifications over a costly foreclosure process. An extremely lengthy foreclosure process, particularly in judicial foreclosure states, also slowed the pace of foreclosed homes hitting the market.

Ironically, the housing market now faces a housing shortage. The decline in foreclosures and shadow inventory has drained the excess supply of existing homes. Meanwhile, existing homeowners trapped with an underwater mortgage are unable to sell, while homebuilders are struggling to ramp up new construction.

This has caused a sharp rise in prices in the housing market, though rising mortgage rates might moderate price gains going forward.

Source: NuWire Investor

Wednesday, July 10, 2013

Will Rising Mortgage Rates Cool the Market?

A big jump in mortgage rates over the past two months may start to cool the rapid rise of home prices in the second half of the year, The Wall Street Journal reports.

Mortgage rates have shot up from lows of 3.59 percent in the beginning of May, to 4.58 percent during the last week of June, according to the Mortgage Bankers Association. Rates are at their highest levels in two years.

“A rule of thumb holds that every one percentage point increase in interest rates reduces affordability by 10 percent, so the recent move in rates just made homes about 10 percent more expensive to buyers who need to finance their purchase,” The Wall Street Journal reports.

Still, economists say mortgage rates at 4.5 percent or 5 percent is still very affordable by historical standards. Merrill Lynch analysts say that home prices would have to rise by 20 percent or mortgage rates would have to soar to around 6 percent to chip away at housing’s affordability.

Some economists see rising mortgage rates as a positive. John Burns, chief executive of John Burns Real Estate Consulting, says that rising rates produce more sustainable price increases. “I don’t think it’s the end of price increases, but I think they’re going to moderate significantly,” Burns told The Wall Street Journal.

Source: “Why Home-Price Gains Will Slow Amid Higher Mortgage Rates,” The Wall Street Journal

Mortgage rates have shot up from lows of 3.59 percent in the beginning of May, to 4.58 percent during the last week of June, according to the Mortgage Bankers Association. Rates are at their highest levels in two years.

“A rule of thumb holds that every one percentage point increase in interest rates reduces affordability by 10 percent, so the recent move in rates just made homes about 10 percent more expensive to buyers who need to finance their purchase,” The Wall Street Journal reports.

Still, economists say mortgage rates at 4.5 percent or 5 percent is still very affordable by historical standards. Merrill Lynch analysts say that home prices would have to rise by 20 percent or mortgage rates would have to soar to around 6 percent to chip away at housing’s affordability.

Some economists see rising mortgage rates as a positive. John Burns, chief executive of John Burns Real Estate Consulting, says that rising rates produce more sustainable price increases. “I don’t think it’s the end of price increases, but I think they’re going to moderate significantly,” Burns told The Wall Street Journal.

Source: “Why Home-Price Gains Will Slow Amid Higher Mortgage Rates,” The Wall Street Journal

Tuesday, July 9, 2013

Falling Inventories and Rising Prices Span Nation to Include California & West Coast

Inventories are declining, and prices are rising, according to a recent report from Movoto Real Estate, a brokerage with a presence in 30 U.S. states.

West Coast cities with the steepest inventory decreases year-over-year in June were Salem, Oregon (-25.4 percent), Bellevue, Washington (-24.5 percent), and Los Angeles (-24.5 percent).

San Jose, California (19.2 percent), and San Diego, California (3.6 percent) were the only two of the 14 cities in the index to experience rising inventories over the 12-month period.

As inventory declines, price per square foot is on the rise. However, the two cities with growing inventories are not left out of this trend. San Diego and San Jose take the second and third places, respectively, in the ranking of cities by price increase over the year.

Price per square foot increased 20.8 percent in San Diego and 18.4 percent in San Jose.

The only city to beat these two was Los Angeles with a 28.6 percent increase. As of last month, the price per square foot for a home in Los Angeles is $432. This is the second-highest price per square foot on Movoto’s June index for the West Coast.

However, San Francisco outpaced all other cities with a price per square foot of $655.

Prices were also generally up over the month, according to Movoto, rising from $251 per square foot to $253 per square foot.

Source: DS News

Examining data from Multiple Listing Services in 34 cities across the nation, Movoto found year-over-year declines in June’s inventory in 32 of the 38 cities it tracks. The most drastic declines took place in Sacramento (-54.5 percent), Detroit (-47.1 percent), and Boston (-46.7 percent).

Over the same time period, price per square foot increased in all but two of the cities Movoto observes. The exceptions were New Orleans (-2.2 percent) and Chicago (-3.2 percent). Sacramento topped the list with a 68.1 percent price-per-square-foot increase.

Highlighting just the West Coast, Movoto found a year-over-year decrease in inventory but a month-over-month increase.

A composite of 14 major metros on the West Coast reveals an 11.9 percent yearly decline in inventory in June, according to Movoto. In contrast, listings rose month-over-month from 12,218 to 13,698.

Over the same time period, price per square foot increased in all but two of the cities Movoto observes. The exceptions were New Orleans (-2.2 percent) and Chicago (-3.2 percent). Sacramento topped the list with a 68.1 percent price-per-square-foot increase.

Highlighting just the West Coast, Movoto found a year-over-year decrease in inventory but a month-over-month increase.

A composite of 14 major metros on the West Coast reveals an 11.9 percent yearly decline in inventory in June, according to Movoto. In contrast, listings rose month-over-month from 12,218 to 13,698.

West Coast cities with the steepest inventory decreases year-over-year in June were Salem, Oregon (-25.4 percent), Bellevue, Washington (-24.5 percent), and Los Angeles (-24.5 percent).

San Jose, California (19.2 percent), and San Diego, California (3.6 percent) were the only two of the 14 cities in the index to experience rising inventories over the 12-month period.

As inventory declines, price per square foot is on the rise. However, the two cities with growing inventories are not left out of this trend. San Diego and San Jose take the second and third places, respectively, in the ranking of cities by price increase over the year.

Price per square foot increased 20.8 percent in San Diego and 18.4 percent in San Jose.

The only city to beat these two was Los Angeles with a 28.6 percent increase. As of last month, the price per square foot for a home in Los Angeles is $432. This is the second-highest price per square foot on Movoto’s June index for the West Coast.

However, San Francisco outpaced all other cities with a price per square foot of $655.

Source: DS News

Monday, July 8, 2013

Researchers: Monetary Policy Not Enough to Prevent Bubbles

National monetary

policy alone cannot reliably prevent or reverse housing bubbles, according to a

recent report from the Lincoln Institute of Land Policy. The downfall lies in

the fact that housing prices and housing markets vary widely across the country,

stated the researchers in the report. Monetary policy and large national

programs such as the Home Affordable Modification Program (HAMP) may help some

markets while hurting others, according to the report, , Preventing House Price Bubbles: Lessons from the 2006-2012 Bust.

Researchers from the Lincoln Institute of Land Policy offer a solution: local countercyclical capital policies.

“The basic idea is straightforward: when prices for a particular asset or sector are rising much faster than market fundamentals justify, bank regulators would increase the capital ratios for that asset,” the researchers explained.

Higher capital reserves make a bank safer and increase mortgage costs, dampening demand, according to the report.

The articles goes on to explain how this solution would help mitigate a the size of the bubble and it does make a good point.

However, they also point out - One of the obstacles to such a policy, the researchers stated, is “there will always be resistance to raising capital requirements when times appear to be good.”

Source: DS News

Researchers from the Lincoln Institute of Land Policy offer a solution: local countercyclical capital policies.

“The basic idea is straightforward: when prices for a particular asset or sector are rising much faster than market fundamentals justify, bank regulators would increase the capital ratios for that asset,” the researchers explained.

Higher capital reserves make a bank safer and increase mortgage costs, dampening demand, according to the report.

The articles goes on to explain how this solution would help mitigate a the size of the bubble and it does make a good point.

However, they also point out - One of the obstacles to such a policy, the researchers stated, is “there will always be resistance to raising capital requirements when times appear to be good.”

Source: DS News

Sunday, July 7, 2013

First-Time Buyers Have Smaller Budget, Interest in Foreclosures

First-time homebuyers tend to work with smaller budgets compared to repeat buyers, which increases the incentive to buy a foreclosure, according to blog from Doorsteps.com, a website that provides information to help potential homebuyers.

Citing a survey from the National Association of Realtors (NAR), the website noted 65 percent of first-time buyers are open to the idea of purchasing a foreclosure despite all of the uncertainties surrounding distressed properties.

Citing a survey from the National Association of Realtors (NAR), the website noted 65 percent of first-time buyers are open to the idea of purchasing a foreclosure despite all of the uncertainties surrounding distressed properties.

In addition, first-time buyers are also more likely to buy a foreclosure compared to a repeat buyer, according to the website.

Doorsteps.com provided three main reasons to explain this. For one, first-time buyers might have more of a reason to seek out discounted properties since they have a smaller budget. According to Doorsteps.com, first-time homebuyers spend an average of $154,100 on a home, which is $65,900 less that repeat buyers, who spend an average of $220,000.

According to the NAR, foreclosures sales offered an average discount of 15 percent compared to non-distressed sales in May.

First-time homebuyers might also have less of a reason to fear the unknown since it is likely they do not know as much about the buying process. In addition, with the abundance of foreclosures, first-time buyers might also view such properties as a “reasonable risk,” the website explained.

Data from Lender Processing Services showed there are a total of 4.56 million properties that are past due (includes delinquencies and foreclosure), of which 1.52 million are in foreclosure inventory as of May.

Source: DS News

Doorsteps.com provided three main reasons to explain this. For one, first-time buyers might have more of a reason to seek out discounted properties since they have a smaller budget. According to Doorsteps.com, first-time homebuyers spend an average of $154,100 on a home, which is $65,900 less that repeat buyers, who spend an average of $220,000.

According to the NAR, foreclosures sales offered an average discount of 15 percent compared to non-distressed sales in May.

First-time homebuyers might also have less of a reason to fear the unknown since it is likely they do not know as much about the buying process. In addition, with the abundance of foreclosures, first-time buyers might also view such properties as a “reasonable risk,” the website explained.

Data from Lender Processing Services showed there are a total of 4.56 million properties that are past due (includes delinquencies and foreclosure), of which 1.52 million are in foreclosure inventory as of May.

Source: DS News

Saturday, July 6, 2013

Asking Home Prices Show Impressive Gain in June, Rents Pick Up

Asking home prices

took off in June, soaring 10.7 percent year-over-year, Trulia reported

Wednesday. Month-over-month, asking prices inched up by 1.5 percent and rose

4.1 percent on a quarterly basis.

Rents rose at a slower pace of 2.8 percent year-over-year, though it was still the biggest increase since January. Trulia also tracked the 100 largest metro areas and revealed 99 markets experienced an increase in asking prices over the last year.

According to Trulia’s chief economist Jed Kolko, the increase in home prices and mortgage rates has added a significant cost to homeownership.

“In the past year, buying a home has become at least 20 percent more expensive,” said Kolko. “For young first-time homebuyers who don’t remember life during and before the bubble, these rising costs are a rude awakening.”

Rents rose at a slower pace of 2.8 percent year-over-year, though it was still the biggest increase since January.

Though, the scenario was reversed in Las Vegas; Oakland, California; and Sacramento, where asking prices shot up by at least 30 percent while rents saw a slight decrease over the last year.

Source: DS News

Rents rose at a slower pace of 2.8 percent year-over-year, though it was still the biggest increase since January. Trulia also tracked the 100 largest metro areas and revealed 99 markets experienced an increase in asking prices over the last year.

According to Trulia’s chief economist Jed Kolko, the increase in home prices and mortgage rates has added a significant cost to homeownership.

“In the past year, buying a home has become at least 20 percent more expensive,” said Kolko. “For young first-time homebuyers who don’t remember life during and before the bubble, these rising costs are a rude awakening.”

Rents rose at a slower pace of 2.8 percent year-over-year, though it was still the biggest increase since January.

Though, the scenario was reversed in Las Vegas; Oakland, California; and Sacramento, where asking prices shot up by at least 30 percent while rents saw a slight decrease over the last year.

Source: DS News

Friday, July 5, 2013

Chino Hills Single Family Home Price Trends

The graph below is the current year-over-year price trend for Chino Hills Original Price vs Sales Prices in Chino Hills. The data was pulled from the Multiple Listing Service (MLS) which is used by all Realtors.

Time frame is from Aug 2012 to Jul 2013

Results calculated from approximately 1,100 listings (Single Family Homes)

If you want the current data for any surrounding areas to include (but not limited to) Diamond Bar, Chino, Pomona, Yorba Linda, Walnut, Corona, Upland or Rancho Cucamonga, call Howard Curry @ 714-323-1233.

Thursday, July 4, 2013

Just Closed Escrow! - Looking to Sell Your House in Chino Hills? Call Howard Curry @ 714.323.1233

Closed escrow on a Chino Hills REO (Fannie Mae - Homepath property) for my Buyers yesterday and in 45 days!

Looking to Buy? I have cash & pre-approved buyers.

If you want to close fast, call Howard Curry 714.323.1233 or visit http://chinohillsresidentialhomes.com/

Looking to Buy? I have cash & pre-approved buyers.

If you want to close fast, call Howard Curry 714.323.1233 or visit http://chinohillsresidentialhomes.com/

Wednesday, July 3, 2013

Report: Housing Market 61% 'Back to Normal'

The housing market made it to 61 percent “back to normal” in May, according to the latest Housing Barometer from Trulia.

May’s percentage is the first time the recovery has passed 60 percent since the crash. April’s barometer was 54 percent. A year ago, the barometer was at only 35 percent.

The monthly report measures three key housing market indicators—construction starts, existing-home sales, and the delinquency-plus-foreclosure rate—to track how quickly the market is recovering to its normal, pre-bubble state.

All three metrics improved in May, with starts and sales rising and the delinquency/foreclosure rate falling.

According to the May report from the Census Bureau, starts were at a seasonally adjusted annual rate of 914,000, up 7 percent from April but still below February and March. On the sales side, the National Association of Realtors reported a 4 percent increase in May to a seasonally adjusted annual rate of 5.18 million.

Overall, starts are about 43 percent back to their normal level of 1.5 million, while sales are 82 percent back to normal.

Meanwhile, the share of mortgages in delinquency or foreclosure dropped to 9.13 percent in May. The combined rate is 57 percent back to normal.

“The recovery has reached full-fledged teenager status, with awkward, sudden growth spurts and parents—the Fed—who now threaten to take away its allowance by winding down measures that pushed mortgage rates down to historic lows,” said Jed Kolko, chief economist at Trulia. “Before long, the recovery should make it into adulthood, but it will face some grown-up challenges in the next couple of years:

1. still-tight mortgage credit for many borrowers,

2. a slow jobs recovery for young adults, and

3. unaffordable housing in large coastal markets.”

Source: DS News

May’s percentage is the first time the recovery has passed 60 percent since the crash. April’s barometer was 54 percent. A year ago, the barometer was at only 35 percent.

The monthly report measures three key housing market indicators—construction starts, existing-home sales, and the delinquency-plus-foreclosure rate—to track how quickly the market is recovering to its normal, pre-bubble state.

All three metrics improved in May, with starts and sales rising and the delinquency/foreclosure rate falling.

According to the May report from the Census Bureau, starts were at a seasonally adjusted annual rate of 914,000, up 7 percent from April but still below February and March. On the sales side, the National Association of Realtors reported a 4 percent increase in May to a seasonally adjusted annual rate of 5.18 million.

Overall, starts are about 43 percent back to their normal level of 1.5 million, while sales are 82 percent back to normal.

Meanwhile, the share of mortgages in delinquency or foreclosure dropped to 9.13 percent in May. The combined rate is 57 percent back to normal.

“The recovery has reached full-fledged teenager status, with awkward, sudden growth spurts and parents—the Fed—who now threaten to take away its allowance by winding down measures that pushed mortgage rates down to historic lows,” said Jed Kolko, chief economist at Trulia. “Before long, the recovery should make it into adulthood, but it will face some grown-up challenges in the next couple of years:

1. still-tight mortgage credit for many borrowers,

2. a slow jobs recovery for young adults, and

3. unaffordable housing in large coastal markets.”

Source: DS News

Tuesday, July 2, 2013

Survey: Agents Expect Prices to Rise, but in Smaller Increments

In concurrence with many industry analysts, real estate agents expect price gains to mellow in the near future, according to survey results released by Redfin, a Seattle-based national brokerage.

Agents also harbor a positive outlook for sellers and a somewhat less positive outlook for buyers in the current market, according to Redfin’s Real-Time Agent Survey of 380 real estate agents.

Eighty-six percent of agents believe prices will rise over the next few months. The same percentage of agents say now is a good time to sell a home. Both of these categories have increased from the first quarter of the year to the second.

However, while a majority of agents expect price gains, a minority expect prices to “rise a lot.” The percent of agents who anticipate prices rising “a lot” in coming months fell from 44 percent in the first quarter to just 16 percent in the second quarter, according to Redfin’s survey.

Factors leading agents to view the current market as a seller’s market include low inventory and an observance of multiple offers on the same homes. Ninety-three percent of agents cited these buyer challenges in Redfin’s survey. While still a significant majority, this is down three percentage points from the first quarter.

On the other hand, the most commonly-cited obstacle for sellers—cited by 40 percent of survey respondents—is low appraisals.

In the current environment, a decreasing percentage of agents are advising buyers to “use aggressive strategies such as waiving contingencies and expanding their budget when facing a bidding war.” About 11 percent of agents admitted to using these strategies, as opposed to 15 percent in the previous quarter.

Source: DS News

Agents also harbor a positive outlook for sellers and a somewhat less positive outlook for buyers in the current market, according to Redfin’s Real-Time Agent Survey of 380 real estate agents.

Eighty-six percent of agents believe prices will rise over the next few months. The same percentage of agents say now is a good time to sell a home. Both of these categories have increased from the first quarter of the year to the second.

However, while a majority of agents expect price gains, a minority expect prices to “rise a lot.” The percent of agents who anticipate prices rising “a lot” in coming months fell from 44 percent in the first quarter to just 16 percent in the second quarter, according to Redfin’s survey.

Factors leading agents to view the current market as a seller’s market include low inventory and an observance of multiple offers on the same homes. Ninety-three percent of agents cited these buyer challenges in Redfin’s survey. While still a significant majority, this is down three percentage points from the first quarter.

On the other hand, the most commonly-cited obstacle for sellers—cited by 40 percent of survey respondents—is low appraisals.

In the current environment, a decreasing percentage of agents are advising buyers to “use aggressive strategies such as waiving contingencies and expanding their budget when facing a bidding war.” About 11 percent of agents admitted to using these strategies, as opposed to 15 percent in the previous quarter.

Source: DS News

Monday, July 1, 2013

Forecast Points to Steady Price Growth Led by California

When it comes to

price appreciation, California markets are expected to continue leading growth

over the next year, while certain markets concentrated in the Northeast should

see a decline in home values, according to Veros Real Estate Solutions' most

recent forecast ending June 1, 2014. The company's forecast covers 969

counties, 324 metro areas, and 13,502 zip codes.

Source: DS News

Source: DS News

Subscribe to:

Posts (Atom)